Desk note N° 003·M&A·6 May 2026

There’s a reason serious M&A deals don’t get announced on a Sunday night.

GameStop’s $56bn unsolicited bid for eBay was the loudest piece of M&A theatre of the year so far. The math doesn’t work, the leverage doesn’t clear, the most credible long walked within 24 hours, and the CEO’s CNBC interview did more damage than the financing letter ever could. But there is a real story underneath the spectacle — and a clean comparison from media M&A six months ago that shows what a credible version of this kind of deal actually looks like.

By Elle Dani · Founder & CIO, els.capital

01 / The set-up

The set-up

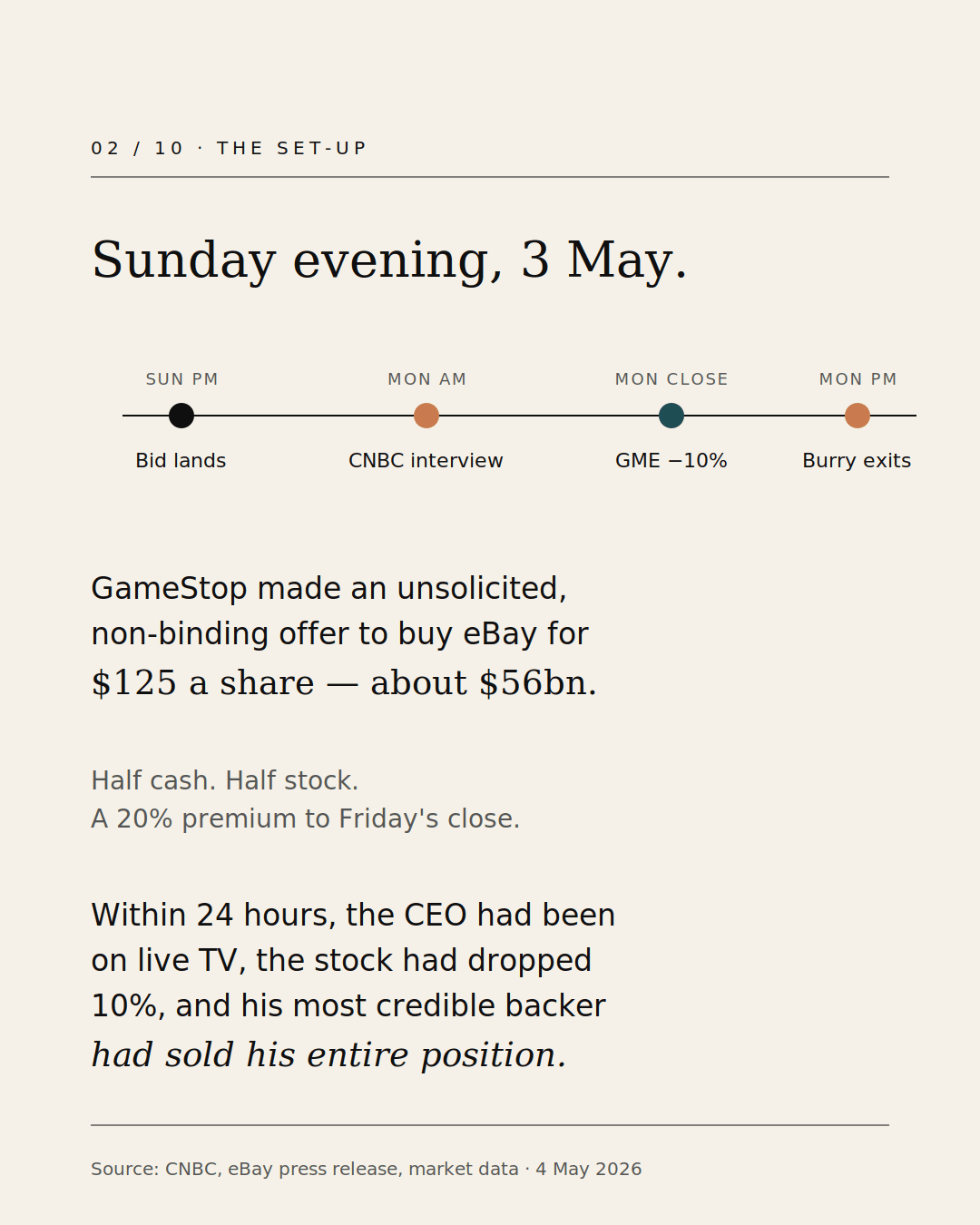

On Sunday evening, 3 May, GameStop made an unsolicited, non-binding offer to acquire eBay for $125 a share — half cash, half stock — valuing the target at roughly $56 billion. The premium was 20% to Friday’s close, 46% to the price before GameStop’s stake-build leaked. TD Bank had reportedly committed up to $20 billion of debt financing.

By Monday’s close, GameStop shares were down 10.14%. eBay had risen, but only to $109.33 — well below the $125 offer. The market’s verdict was visible in real time on the same screen the CEO was being interviewed on.

02 / The mismatch

The mismatch

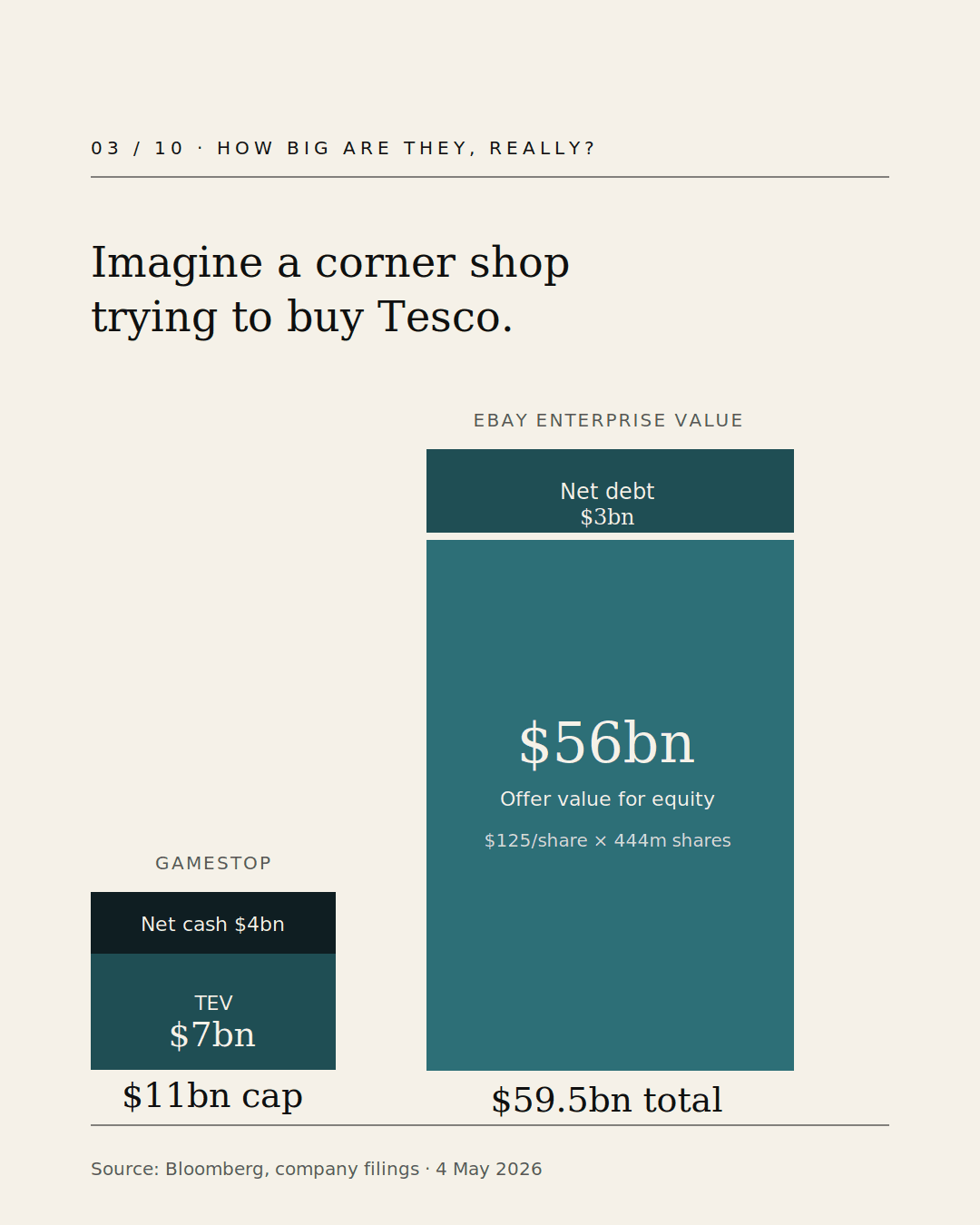

Begin with the picture. GameStop has a market capitalisation of approximately $11 billion. eBay’s offer-implied enterprise value is $59.5 billion ($56bn equity offer plus ~$3bn net debt). The buyer is roughly one-fifth the size of the target.

This is unusual but not unprecedented. Smaller bidders have eaten larger targets before, almost always in two ways: through structurally credible financing — typically with a deep-pocketed strategic backer — or by trading equity at a level that gives selling shareholders comfort about the combined entity. Neither has been articulated here.

03 / Why the math doesn’t work

Why the math doesn’t work

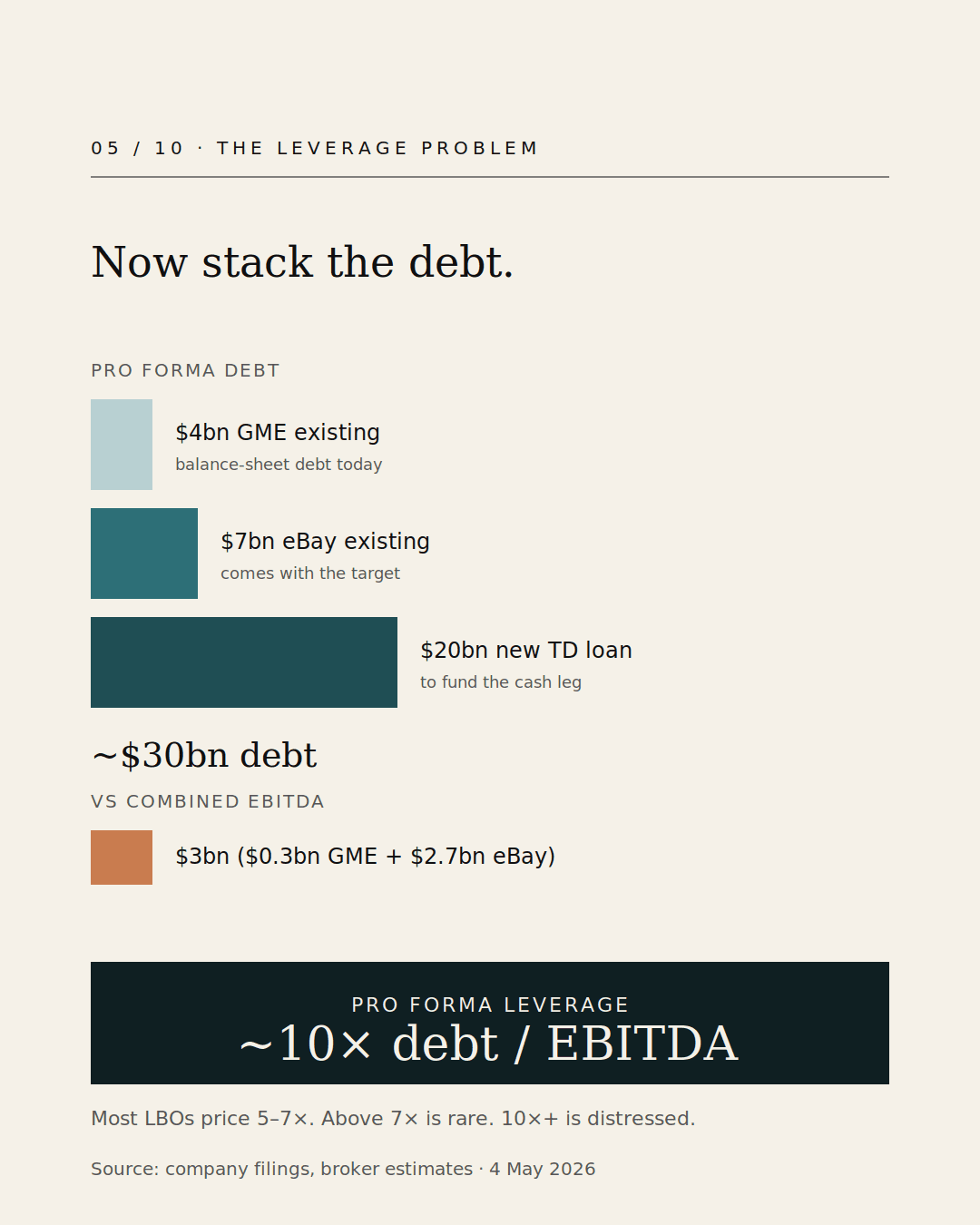

The cash leg is plausible on the surface and dangerous underneath. GameStop has approximately $9 billion of cash on the balance sheet. Add the $20 billion TD facility and you get $29 billion — sufficient to fund the $28 billion cash component. Tight, but it works.

The problem is what’s left on the pro-forma balance sheet. Combining GameStop’s existing $4 billion of debt, eBay’s $7 billion, and the new $20 billion TD facility produces roughly $30 billion of total debt. Against a combined EBITDA of approximately $3 billion — $0.3 billion from GameStop and $2.7 billion from eBay — that is leverage of approximately ten times.

Most LBOs price between five and seven times. Anything above seven is rare. Ten times and above is distressed-debt territory. There is no operationally-credible path to deleveraging this combination in the medium term — eBay is a mature, low-growth marketplace, GameStop is a structurally challenged retailer, and the combined synergy case has not yet been articulated by anyone on the buy-side.

04 / The Burry exit

The Burry exit

Within 24 hours of the bid, Michael Burry sold his entire GameStop position — his first full sale since launching his Substack — and explained why in plain language.

Never confuse debt for creativity. The Instant Berkshire thesis was never compatible with greater than 5× Debt/EBITDA, never ok with interest coverage under 4.0×.

— Michael Burry, Substack, 4 May 2026

Burry had been the most credible value-investor in the GameStop story, a public proponent of the so-called “Instant Berkshire” thesis. His exit removes the intellectual scaffolding that kept the equity case respectable. It does not kill the deal. It does, however, narrow the universe of long-only institutional investors prepared to fund the stock leg at the offer price.

05 / The interview

The interview

On Monday morning Cohen appeared on CNBC’s Squawk Box. Andrew Ross Sorkin asked the question every hostile bidder must be able to answer:

How does the math work for you, given the price tag of $56 billion, given the market cap of GameStop?

— Andrew Ross Sorkin, CNBC, 4 May 2026

Cohen’s response — repeated three times across the segment — was: “I don’t understand your question.”

He did not name a strategic partner. He did not articulate an equity backstop. He did not explain how the cash gap would close, how the dilution from the stock leg would be calibrated, or why eBay shareholders should accept a paper currency now backed by ten-times leverage. He repeated, instead, that he was “aligned with shareholders.”

Alignment is an input. Accretion-and-dilution math is an output. Sorkin asked for the output. The CEO declined to provide it.

06 / How this is supposed to be done

How this is supposed to be done

A small buyer pursuing a much bigger target is not, in itself, a flawed transaction structure. It happened in media six months ago.

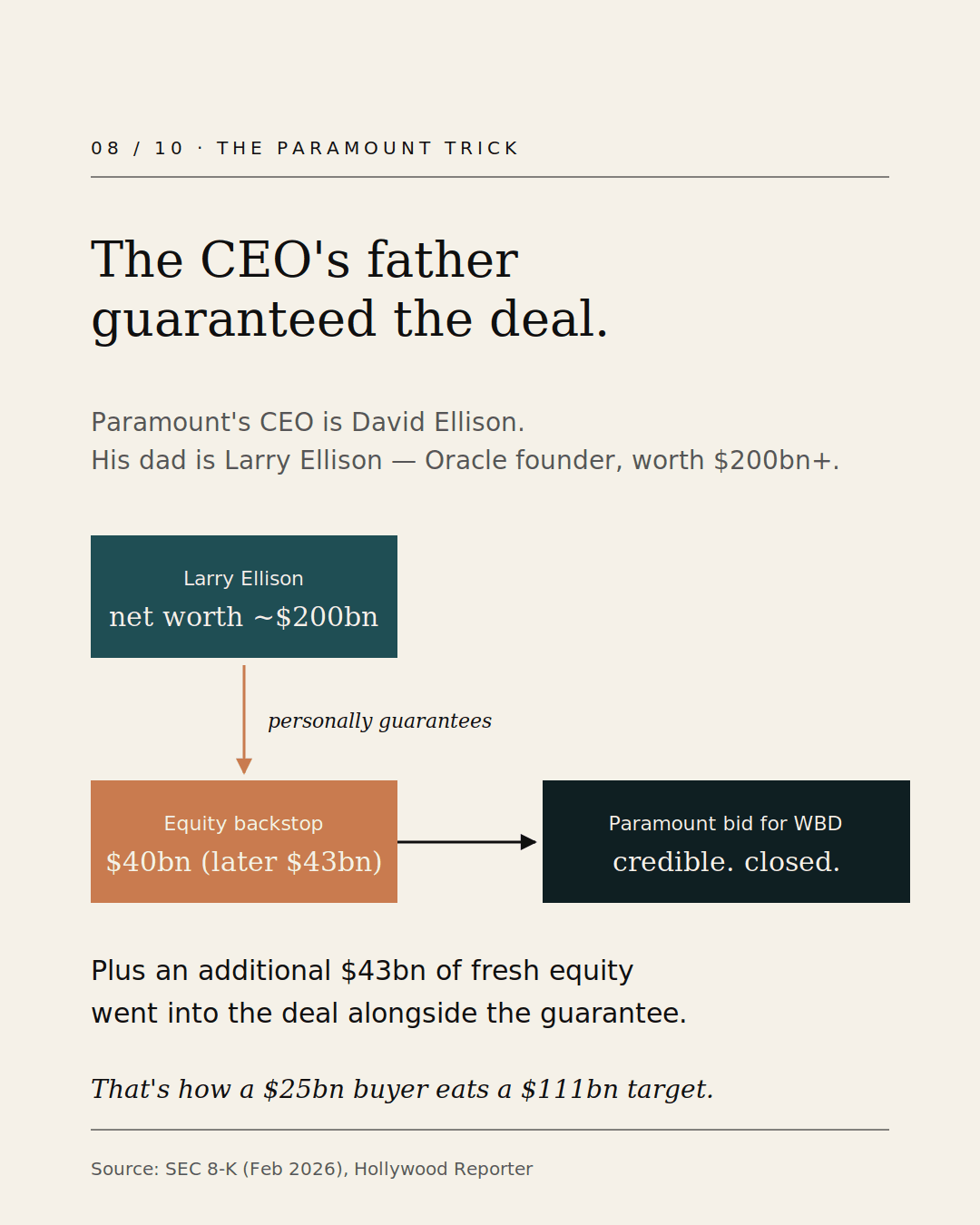

In December 2025, Paramount Skydance — a $25 billion company — won an auction for Warner Bros. Discovery with an offer that valued the target at $111 billion. The buyer was roughly four times smaller than the prize. The bid won.

It won because the financing was credible. Paramount’s CEO is David Ellison. His father is Larry Ellison, founder of Oracle, with a personal net worth above $200 billion. To address concerns from the WBD board, Larry Ellison provided an irrevocable personal guarantee for $40.4 billion of the equity financing, anchored against approximately 1.2 billion Oracle shares held in the Ellison family trust. The guarantee was later raised to $43.3 billion in the February 2026 amendment.

That is the template. A guarantor with a balance sheet that dwarfs the deal. Documentation filed with the SEC. A trust frozen for the duration of the transaction. A break fee raised to match the rival bid. Each element designed to remove a specific reason a target board could refuse to engage.

On Squawk Box, Cohen mentioned none of these things. There was no strategic backer named, no personal commitment offered, no alternative cash structure floated. The contrast with the Paramount precedent is not subtle. It was the question being asked.

07 / House view

House view

Three theories are circulating about what GameStop is actually doing:

- 1 —

CEO compensation hurdle. Cohen’s pay package reportedly unlocks if GameStop’s market capitalisation clears $20 billion. A bid that triples the perceived total addressable market does, mechanically, push the share price toward that hurdle.

- 2 —

Mark-to-market on derivatives. GameStop holds approximately 5% of eBay, mostly via options. Acquisition speculation produces favourable mark-to-market on that derivative book regardless of whether the deal closes.

- 3 —

Putting one of them in play. A public, headline-grabbing bid forces strategic alternatives onto the eBay board and may attract a counter-bidder for either company.

Each theory rationalises the bid as a derivative play rather than a closing transaction. None requires the math to work in the conventional sense. All are consistent with a CEO declining, three times on live television, to engage with the financing question.

Our view

This is not a bid structured to close. It is a bid structured to be announced.

Probability of consummation in the offered form is, in our judgment, very low. Probability of a structurally renegotiated transaction — at a lower headline price, with strategic-partner financing and a more equity-heavy mix — remains non-zero, conditional on Cohen finding a guarantor of meaningful size. Without one, the most likely outcome is withdrawal, with a residual mark-to-market benefit on the derivative position and a market-cap re-rating that may or may not survive the cycle.

The takeaway

Hostile bids live or die on whether the bidder can convince the target’s shareholders to override their own board. That requires credibility — a backstop, a guarantor, a structure. Not combativeness. Not alignment. Not reframing the obvious question as one you don’t understand.

The financing question doesn’t get easier with bigger zeros. It gets harder.

Source documents

- CNBC Squawk Box transcript, 4 May 2026.

- Michael Burry, Substack, 4 May 2026.

- Paramount Skydance Form SC TO-T/A and Form 8-K (Ellison Guarantee, Exhibit 10.1), SEC Edgar, December 2025 – February 2026.

- eBay press release confirming receipt of GameStop’s offer, 4 May 2026.

© els.capital 2026 · Informational purposes only · Not investment advice.